Cross currency pairs sit at the intersection of macro themes and relative performance, helping traders to focus on how one economy is performing against another rather than against the US dollar. A well-constructed cross currency pairs list acts as a decision tool: it helps prioritise which regional stories, policy divergences, or risk cycles are most tradeable at any given time, rather than reacting to every move in USD-led markets.

Quick summary

- Cross-currency pairs exclude USD and reflect regional themes rather than US data.

- They can improve diversification, hedge USD exposure, and express macro views directly.

- Spreads are often wider and liquidity more session-dependent than USD majors.

- A structured workflow—pair selection, session timing, risk sizing, and journalling—is essential.

Trading forex involves significant risk and may not be suitable for all traders. Losses can exceed initial expectations, especially when leverage is involved.

What is a cross-currency pair list in forex trading, and why does it matter?

A cross currency pairs list is a curated watchlist of non-USD forex pairs that a trader actively follows for analysis and trade ideas. Instead of scanning the entire market, the list narrows attention to pairs that best reflect specific regional relationships—such as Europe versus the UK or Asia-Pacific risk dynamics—making analysis more focused and repeatable.

It matters because most major pairs are heavily influenced by US economic data and Federal Reserve policy. Crosses allow you to target regional fundamentals directly, such as European inflation, UK growth, Japanese monetary policy, or commodity cycles in Australia and Canada—without routing exposure through USD.

What key terms should traders know when trading currency crosses?

- Major pairs: USD-based pairs with high liquidity and tight spreads.

- Minor pairs (crosses): Non-USD pairs with moderate liquidity and wider spreads.

- Exotic pairs: One major currency paired with an emerging-market currency; higher risk and cost.

- Spread: Difference between bid and ask prices.

- ATR (Average True Range): A volatility measure used for position sizing and stop placement.

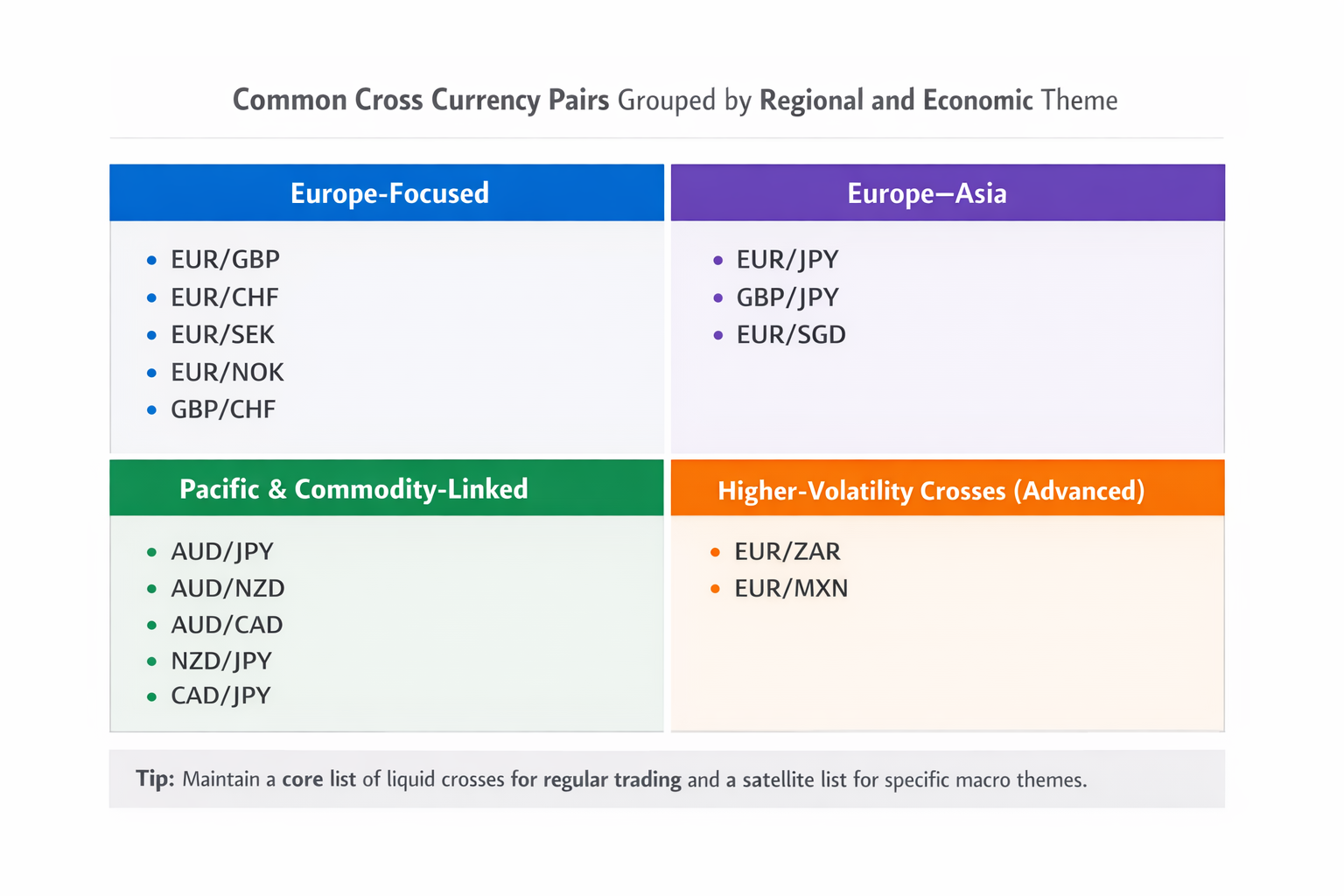

Which forex cross pairs commonly appear on a cross-currency pairs list?

Below is an illustrative list grouped by theme. Availability varies by platform.

Europe-focused

EUR/GBP, EUR/CHF, EUR/SEK, EUR/NOK, GBP/CHF

Europe–Asia

EUR/JPY, GBP/JPY, EUR/SGD

Pacific and commodity-linked

AUD/JPY, AUD/NZD, AUD/CAD, NZD/JPY, CAD/JPY

Higher-volatility crosses (advanced)

EUR/ZAR, EUR/MXN

Tip: Maintain a core list of liquid crosses for regular trading and a satellite list for specific macro themes.

“When traders move beyond USD majors, the key is not quantity but relevance. A focused cross-currency pairs list aligned to regional themes tends to produce cleaner signals and better risk control.” — Deriv market analyst

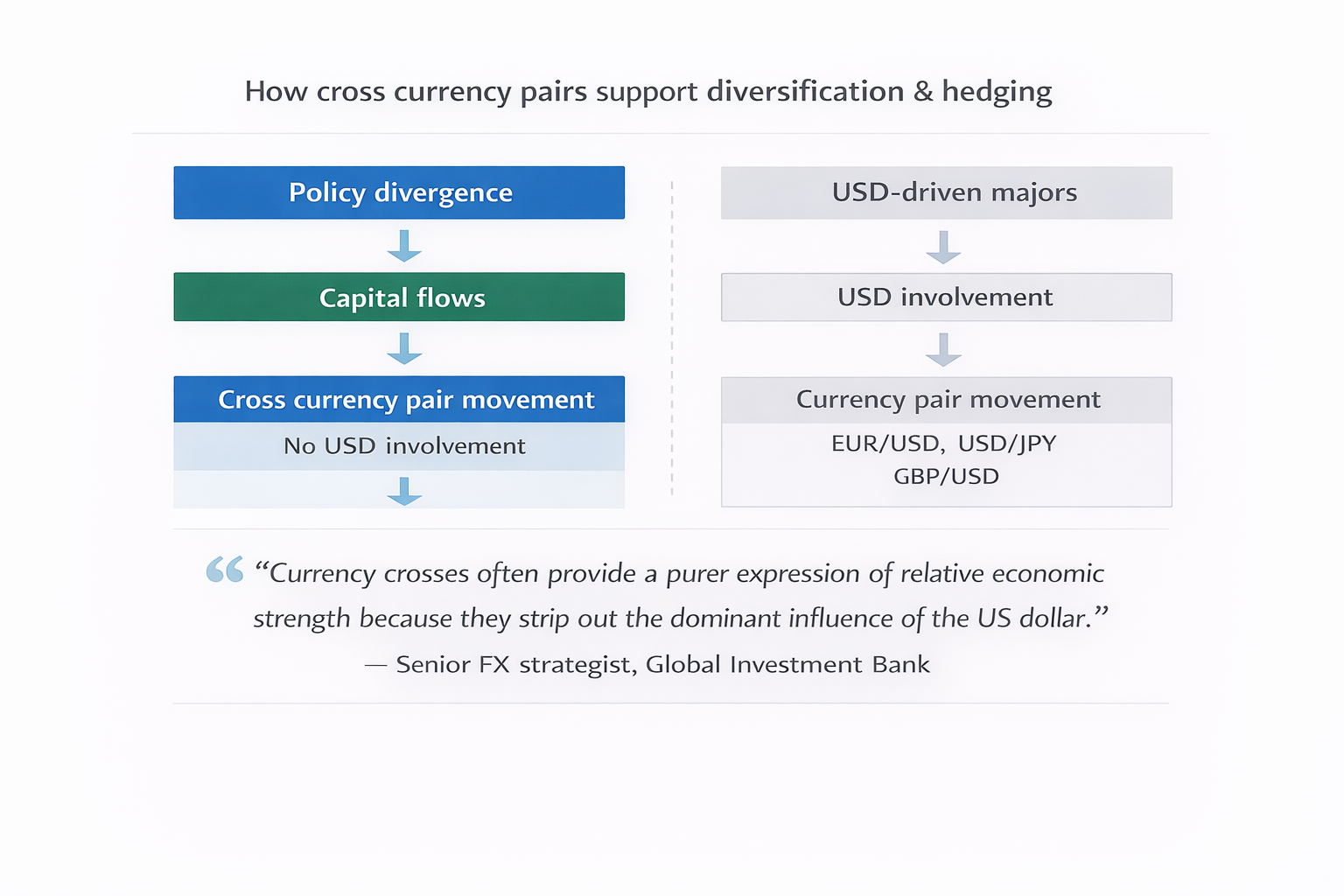

How does cross-currency trading support forex diversification and hedging?

Beyond basic diversification, a well-maintained cross-currency pairs list helps traders separate regional narratives that are often blurred in USD majors. When global markets are dominated by US data releases, interest-rate expectations, or shifts in Federal Reserve guidance, non-USD pairs can continue to reflect local economic realities. This separation is particularly valuable during periods of heightened US volatility, when USD-driven moves can distort signals in major pairs.

Crosses also allow traders to express relative-value views between economies at similar stages of the business cycle. For example, comparing two developed markets with differing inflation pressures or fiscal outlooks can produce more stable trends than pairing one developed economy with the USD. Over time, this approach may help traders manage behavioural tendencies, such as overtrading around US news or abandoning valid setups.

In practice, diversification through crosses is most effective when traders are conscious of USD concentration risk. During periods of elevated US volatility, such as Federal Reserve rate decisions or major inflation releases, USD majors often move in unison, reducing the benefit of holding multiple positions that appear diversified on the surface. A curated cross-currency pairs list helps avoid this trap by shifting focus to relative performance between two non-USD economies.

“Currency crosses often provide a purer expression of relative economic strength because they strip out the dominant influence of the US dollar.” — Senior FX strategist, global investment bank

Another advantage is the ability to manage correlation drift. Relationships between currencies are not static; pairs that once moved independently can become highly correlated during global risk events or policy convergence. Regularly reviewing how crosses behave relative to USD majors allows traders to rotate pairs in and out of their core list as market regimes change. This adaptability is difficult to achieve when trading only a narrow set of USD-based pairs.

From a practical standpoint, traders often use crosses as part of a broader approach to managing exposure to volatility. When US data dominates headlines and price action becomes erratic, regional crosses may continue to respect technical structure driven by local fundamentals. Over time, this can reduce behavioural errors such as overtrading around US news or abandoning valid setups due to short-term USD noise.

Diversification

Crosses are driven by distinct macro forces such as regional growth, inflation paths, and commodity demand. For example, EUR/SEK may react to ECB versus Riksbank guidance, while AUD/JPY often tracks risk sentiment and commodity prices.

A simple check is to review rolling correlations between your positions. Crosses with low correlation to USD majors can help smooth portfolio volatility when US data dominates markets.

Hedging

If your book is concentrated in USD pairs, crosses can reduce sensitivity to US events. For instance:

- Long EUR/GBP expresses euro strength versus sterling without USD exposure.

- A small position in a cross can partially offset USD risk ahead of major US data releases.

Hedges are never perfect, but they can reduce drawdowns during periods of USD volatility.

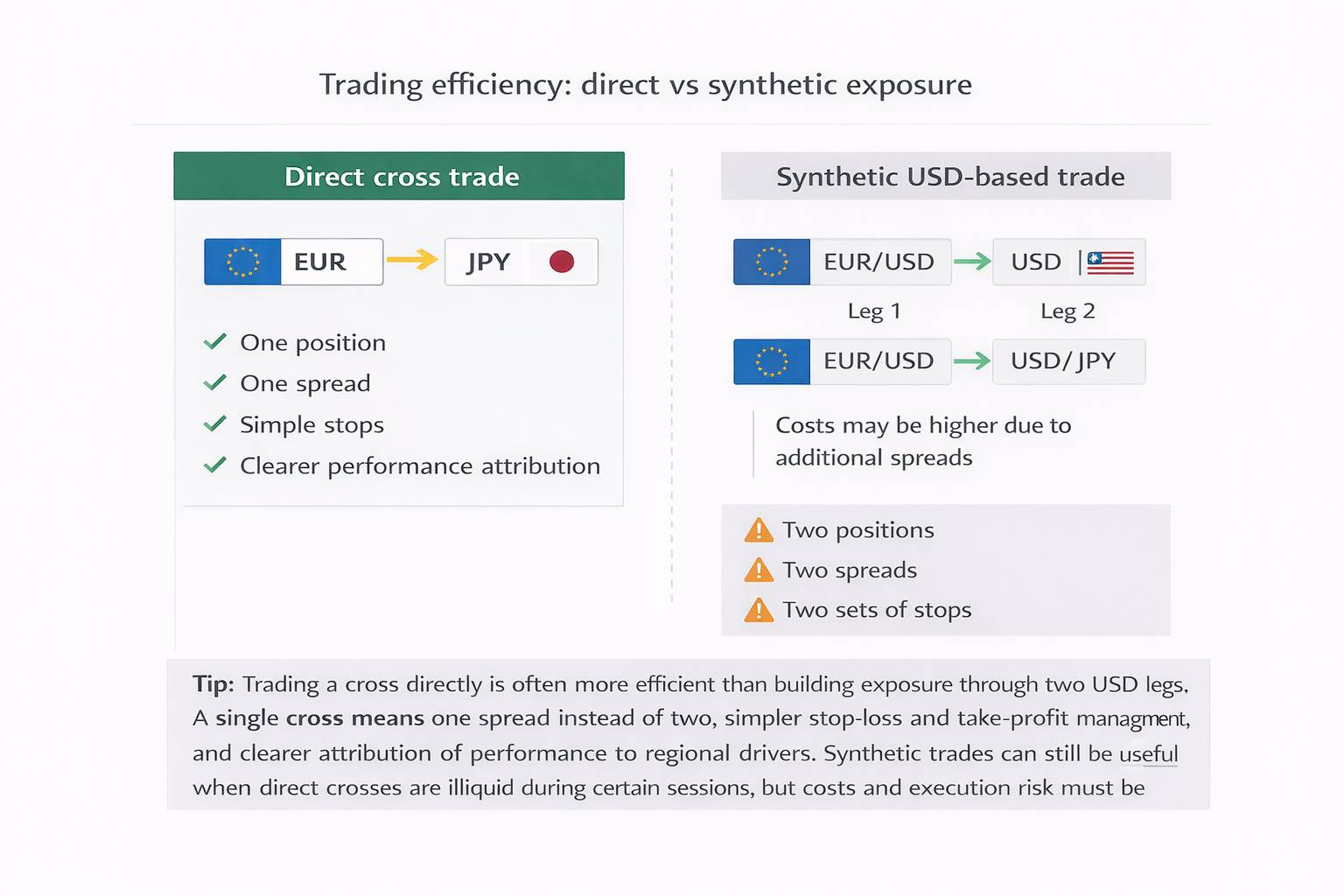

Is trading currency crosses more efficient than trading synthetic USD?

Expert insight (Deriv): “From a trading perspective, direct crosses can reduce operational complexity at the execution level. One position is easier to manage than two synthetic legs, especially during fast markets.” — Deriv trading specialist

- One spread instead of two.

- Simpler stop-loss and take-profit management.

- Clearer attribution of performance to regional drivers.

Synthetic trades can still be useful when direct crosses are illiquid during certain sessions, but costs and execution risk must be monitored carefully.

How do carry, spreads, and sessions affect cross-currency trading?

Funding costs and carry dynamics play a more visible role in cross-currency trading than many traders initially expect. Because each cross reflects the interest-rate policies of two non-USD central banks, overnight financing can either support or slowly erode performance over time. Even trades with correct directional bias may underperform if negative carry is ignored.

For traders holding positions over several days, it is useful to align the expected duration of the trade with the carry profile of the pair. Short-term technical setups may justify tolerating negative carry, while swing or position trades generally benefit from carry-neutral or carry-positive crosses. Monitoring swap schedules and being aware of higher-cost rollover days helps avoid surprises.

Carry considerations also interact closely with volatility and trade duration. For intraday traders, overnight financing may be irrelevant, allowing greater flexibility in pair selection. For swing traders, however, persistent negative carry can significantly impact performance, especially when positions are held through periods of low volatility, where price progress is slow. In such cases, even a technically sound trade can underperform once financing costs are taken into account.

Session timing further amplifies this effect. Positions opened during illiquid hours may face wider spreads and less favourable rollover pricing, increasing the effective cost of holding the trade. Aligning entry timing with the most active session for the pair not only improves execution quality but also helps ensure that expected price movement is sufficient to justify funding costs. This is why many experienced traders align cross-selection, session timing, and holding period as part of a single decision-making process rather than treating them independently.

Liquidity conditions also vary meaningfully across sessions. Outside core trading hours, market depth can thin, spreads may widen, and stop execution can deteriorate. Incorporating session awareness into trade planning is therefore as important as technical analysis itself.

Crosses inherit interest-rate differentials from both currencies. Before holding positions overnight:

- Check whether carry is positive or negative.

- Be aware of triple-swap days.

- Align holding period with carry expectations.

Liquidity is also session-dependent. EUR/GBP trades best during London hours, while AUD/JPY is most active during Tokyo and Sydney sessions. Outside core hours, spreads can widen significantly.

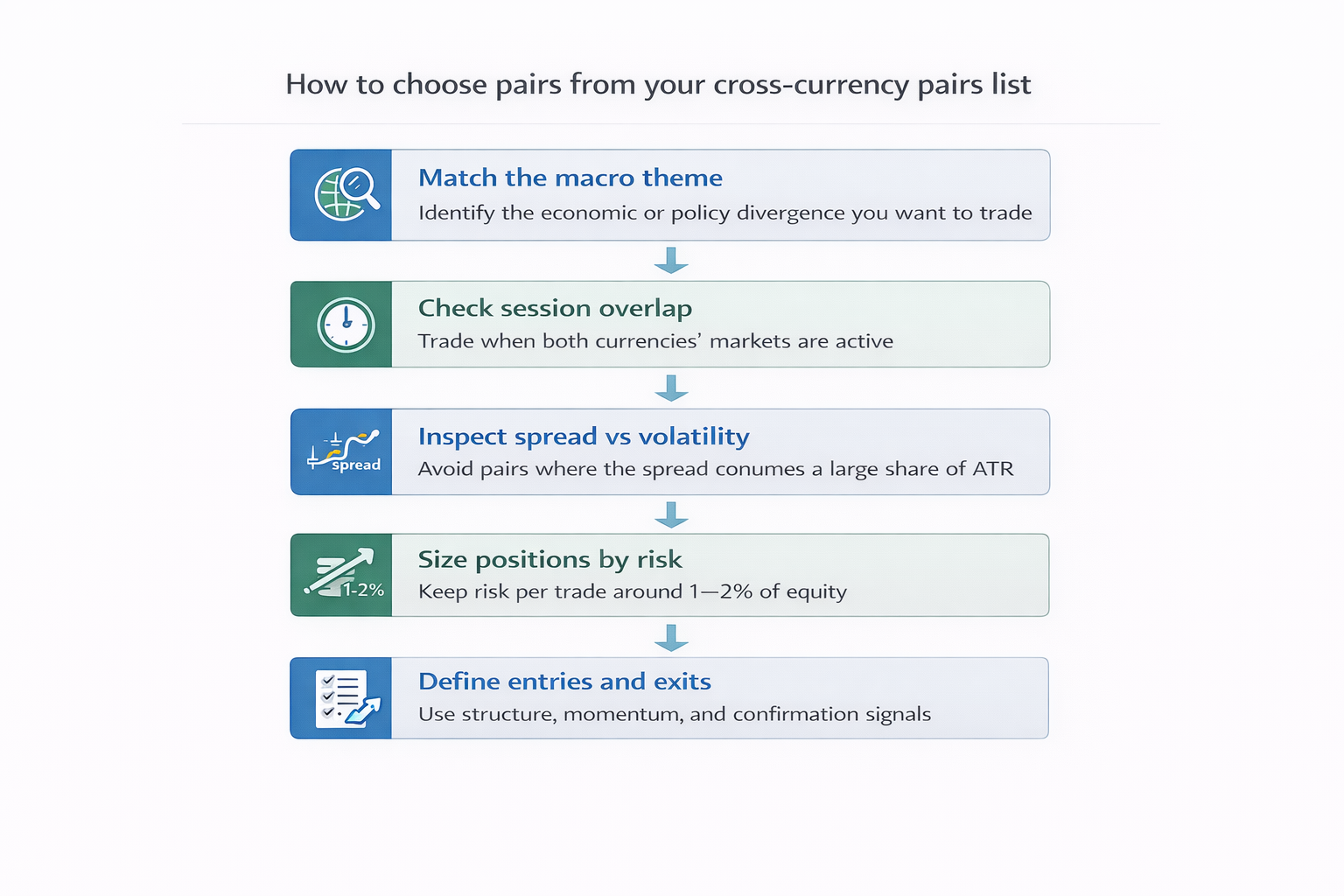

How should traders choose pairs from a cross-currency pairs list?

Use this five-step framework:

- Match the macro theme: Identify the economic or policy divergence you want to trade.

- Check session overlap: Trade when both currencies’ markets are active.

- Inspect spread vs volatility: Avoid pairs where the spread consumes a large share of ATR.

- Size positions by risk: Consider risk per trade around 1–2% of equity as a guideline. Define entries and exits: Use structure, momentum, and confirmation signals.

What risks affect minor currency pairs, and how should traders manage them?

Effective risk management is what can turn a cross-currency pairs list from a collection of instruments into a repeatable trading framework. Because volatility and liquidity vary widely across crosses, applying identical position sizes or stop distances can lead to inconsistent outcomes. Normalising risk across trades helps ensure that no single position dominates portfolio performance.

Another common risk is theme clustering, where multiple positions are driven by the same underlying factor. Holding EUR/JPY and GBP/JPY simultaneously, for example, may appear diversified but often results in heavy exposure to Japanese yen risk sentiment. Treating related crosses as a single risk bucket—and capping total exposure accordingly—helps prevent drawdowns caused by one macro shock affecting several positions at once.

In practice, this means adjusting exposure based on both average volatility and execution conditions. A relatively calm cross traded during its most liquid session may justify tighter stops and standard sizing, while a thinner pair traded off-session may require reduced size and wider invalidation levels. These adjustments are not signs of uncertainty; they are deliberate controls intended to limit downside exposure.

“Wider spreads do not make cross-currency pairs inherently riskier; poor sizing does. Volatility-adjusted position sizing is what keeps risk consistent.” — Independent risk management consultant

- Size positions using ATR, not conviction.

- Place stop-losses beyond clear invalidation levels, not round numbers.

- Limit exposure to a single macro theme.

- Reduce risk ahead of major data releases affecting either currency.

Consistent journalling—tracking spread, session, rationale, and outcome—helps identify which crosses behave best in your trading hours.

What are common trading setups using forex cross pairs?

EUR/GBP range trade

- Context: Well-defined range during stable policy expectations.

- Plan: Buy near support, sell near resistance, with tight invalidation.

EUR/JPY momentum trade

- Context: Policy divergence and improving risk sentiment.

- Plan: Enter on a break-and-retest basis, managing with a trailing stop.

These examples illustrate structure and risk control, not trade signals.

How do currency crosses compare with USD major pairs?

Understanding how crosses differ from USD majors helps traders decide when each category is most appropriate. USD majors often provide deeper liquidity and lower transaction costs, making them suitable for high-frequency or news-driven strategies. Crosses, by contrast, are better suited to traders who prioritise thematic clarity and medium-term positioning.

Rather than choosing one category exclusively, many traders use USD majors as a liquidity anchor while deploying crosses selectively to express more nuanced macro views. This blended approach balances cost efficiency with strategic flexibility and reduces reliance on a single dominant driver.

- Drivers: Crosses reflect two non-USD economies; majors are USD-centric.

- Costs: Crosses usually have wider spreads.

- Use case: Crosses suit diversification and targeted macro views; majors anchor liquidity.

Most traders benefit from using both.

How can beginners get started with a cross currency pairs list?

- Build a watchlist aligned to your trading session.

- Practise on a demo account before committing capital.

- Select account settings that align with your holding period.

- Start with small position sizes and refine your approach through review and risk monitoring.

Quiz

What is a cross-currency pair?

FAQs